Ownership intelligence

2026 Family Car Ownership Cost Calculator

Calculate the true 5-year ownership cost of family cars in India. Compare fuel, maintenance, and resale values for 2026. Save up to ₹2 Lakh with data-backed recommendations.

Enter Your Requirements

Three quick steps — same calculator engine underneath.

The Down Payment Reward Strategy

Why use a debit card for a ₹4L–₹8L payment? Swiping the right credit card can fund your first family vacation before the car even hits the road. Estimated Gain: ₹25,000 – ₹50,000.

Budget band up to ₹20,00,000: many buyers plan roughly ₹4,00,000–₹8,00,000 down (about 20–40% — adjust for your loan and dealer).

Amex Platinum Travel

Ideal for a ₹4 Lakh down payment.

Estimated Gain

₹32,000+

Taj Voucher + 48k MR Points

- ✅ Triggers all milestones in ONE swipe.

- ✅ Transfer points to Marriott/Airlines.

Axis Magnus

Best if Down Payment > ₹2 Lakhs.

Estimated Gain

₹25,000+

4% - 6% Effective Reward Rate

- ✅ Thrives on monthly milestones.

- ✅ Premium concierge & travel perks.

SBI Cashback Card

Flat 1% Offline / 5% Online.

Estimated Gain

₹5,000

Direct Statement Cashback

- ✅ Simple “cash-in-bank” model.

- ✅ Ideal for accessories & insurance.

Amex Platinum Travel

Ideal for a ₹4 Lakh down payment.

Estimated Gain

₹32,000+

Taj Voucher + 48k MR Points

- ✅ Triggers all milestones in ONE swipe.

- ✅ Transfer points to Marriott/Airlines.

Axis Magnus

Best if Down Payment > ₹2 Lakhs.

Estimated Gain

₹25,000+

4% - 6% Effective Reward Rate

- ✅ Thrives on monthly milestones.

- ✅ Premium concierge & travel perks.

SBI Cashback Card

Flat 1% Offline / 5% Online.

Estimated Gain

₹5,000

Direct Statement Cashback

- ✅ Simple “cash-in-bank” model.

- ✅ Ideal for accessories & insurance.

⚠️ The 1.18% Surcharge Alert

Most dealers charge a 1.5–2% fee. Only swipe if your reward value (e.g., Amex at 8%) is higher than the fee. Pro-tip: Pay via an Online Link if possible to avoid offline surcharges.

💡 The Credit Limit Hack

Low limit? Pre-pay your card bill by the extra amount (e.g., pay ₹2L into a ₹3L limit card) to create a “Negative Balance” and swipe for ₹5L instantly.

Educational only. Rewards, caps, and merchant eligibility change. Confirm down payment card acceptance, fees, and T&C with your dealer and the issuer before you pay. Apply links may be affiliate links — we may earn a commission at no extra cost to you.

Frequently Asked Questions (2026)

What is the break-even point for Hybrid vs EV in India 2026?

In 2026, with petrol at ₹108/L and EV charging at ₹9/unit, the break-even point typically occurs at 12,000-15,000 km annual driving. For city-heavy usage, EVs become more economical after 3-4 years due to lower running costs. However, hybrid vehicles offer better value for mixed usage patterns and don't require charging infrastructure. Our calculator factors in 2026 fuel prices to show the true break-even point for your usage.

How do Bharat NCAP ratings affect car resale value in 2026?

Bharat NCAP ratings significantly impact resale value. Cars with 4-5 star ratings retain 5-10% more value after 5 years compared to lower-rated vehicles. Our calculator accounts for safety ratings in both the recommendation score and resale value calculations. Premium safety features like 6+ airbags and ESC systems are now standard expectations for family cars in 2026.

What is the expected resale value of petrol vs hybrid vs EV after 5 years in 2026?

Based on 2026 market trends: Petrol cars from trusted brands (Toyota, Honda, Maruti) retain 60-70% value. Hybrid vehicles maintain 65-75% resale value due to strong demand. EVs show 55-65% retention, with battery health being a key factor. Our calculator uses brand-specific resale multipliers that reflect current market conditions and account for the growing preference for fuel-efficient vehicles.

How does road tax vary by state and affect total ownership cost?

Road tax varies significantly by state/UT in India, ranging from 10% (Delhi) to 18% (Karnataka). This can add ₹50,000-₹3.6 Lakh to the on-road price depending on your location and car value. Our calculator includes a state selector to provide accurate on-road price calculations. The 5-year ownership cost formula accounts for these regional variations: Total Cost = On-road Price + Fuel (5 years) + Insurance (5 years) + Maintenance (5 years) - Resale Value.

What is the impact of CAFE III norms on diesel car pricing in 2026?

CAFE III (Corporate Average Fuel Economy) norms effective from 2026 require stricter emission standards, increasing diesel vehicle manufacturing costs by 2-4%. This makes hybrid and EV options more competitive. Our calculator reflects these market dynamics in the ownership cost projections, helping you make informed decisions based on current regulatory environment.

Can I pay a car down payment with a credit card in India? (2026 Rules)

Yes, you can pay a car down payment using a credit card at most Indian dealerships (Maruti, Hyundai, Tata, etc.). While dealers typically levy a 1.5% to 2% surcharge on credit cards for car purchase 2026, savvy buyers use Milestone Cards like Amex Platinum Travel to generate an 8% value-back. This creates a 6% Net Profit, effectively earning you over ₹30,000 on a ₹5 Lakh swipe.

The credit card for car down payment India 2026 strategy works best when your reward yield (milestone value ÷ swipe amount) clearly exceeds the dealer surcharge. Use the Smart Buyer's dashboard above to verify your net profit before heading to the showroom. Separately, the best credit card for car insurance premium 5% cashback is the SBI Cashback Card — insurance has zero surcharge, so the 5% is pure profit. These are two independent levers of the car loan vs credit card down payment arbitrage strategy that can collectively save ₹25k–₹50k on a single car purchase.

🚗 Car Buying Savings Guide (Save ₹2–5 Lakh)

These expert tips from real car buyers in India 2026 will help you save ₹1.26L–₹2.64L across five phases — before, during, and after purchase — alongside your 5-year TCO results. For a quick video overview.

Quick Savings Checklist

Tick items off as you prepare for the dealership.

- Compared total car cost vs 25% of take-home (EMI + fuel + insurance + maintenance)

- Chosen purchase timing (festive, quarter-end, or off-season)

- Checked road tax in your state vs neighbouring states

- Collected 2–3 bank loan pre-approvals

- Negotiated full on-road price, not just ex-showroom

- Declined or repriced dealer add-ons

- Sourced insurance outside the dealer when cheaper

- Asked for free or discounted service package / voucher

- Used competing dealer quotes as leverage

- Planned down payment and shortest sensible loan tenure

- Shortlisted a fuel cashback card for after purchase

- Planned service records and resale window (often years 4–5)

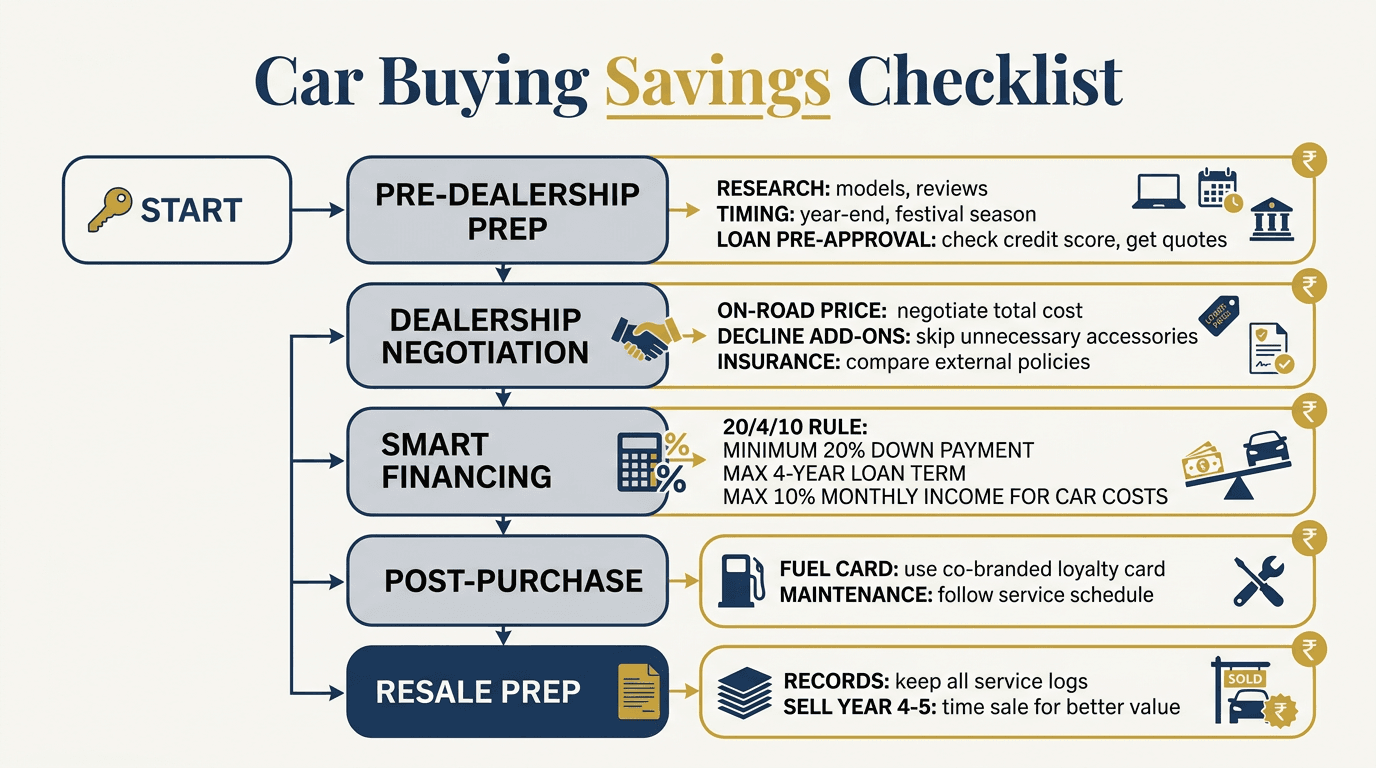

Car Buying Savings Checklist

Visual flow from prep → negotiation → financing → ownership → resale.

Run the advisor above until you see results, then use Download PDF — your export includes the full three-page Insider Car Buying Tips appendix (checklist + flowchart).

FreeFuelBill tools

- Fuel Credit Card Guide — compare top cards and cashback

- Fuel Cost Calculator — project spend with your mileage

- Fuel Expense Tracker — track monthly fuel spend and trends (Fuel Analytics)

- Fuel Expense Documentation Guide — audit-ready records

Car buying savings FAQs

What's the best time to buy a car in India?

Festive seasons such as Diwali often bring higher discounts and bundled offers; month- and quarter-ends (March, June, September, December) can improve negotiation because sales targets matter. Monsoon or low-traffic months sometimes mean quieter showrooms and better attention. Avoid assuming the same calendar every year — combine timing with on-road price quotes from multiple dealers.

How much should I spend on a car?

A common guardrail is to keep all car-related spending within about 25% of monthly take-home income (EMI, fuel, insurance, servicing). Your advisor shows a monthly equivalent (5-year TCO ÷ 60) — check that it fits your budget alongside other goals, and prefer a healthy down payment with the shortest sensible loan tenure you can afford.

How do I negotiate car prices with dealers?

Ask for the best on-road or out-the-door price including taxes, registration, insurance, and fees — not just ex-showroom. Use written quotes from other dealers, refuse overpriced add-ons, compare insurance outside, and negotiate service benefits before you sign. Walking away is often your strongest lever.

How to Use the Family Car Decision Advisor

Expand

Our Family Car Decision Advisor helps you pick a car and an efficient payment plan by calculating true 5-year ownership cost (TCO) for your state and your usage. Follow these steps:

- Enter Family Size: Specify the number of family members. The advisor filters cars with adequate seating capacity (5-seater for up to 4 members, 7-seater for larger families).

- Set Budget Range: Enter your minimum and maximum budget. This helps narrow down options within your price range. Consider on-road prices (ex-showroom + taxes + registration).

- Select Usage Type: Choose city, highway, or mixed driving. City driving typically has lower mileage, while highway driving is more fuel-efficient. Mixed usage provides a balanced average.

- Choose Fuel Preference: Select petrol, diesel, hybrid, EV, or any. Each fuel type has different running costs and maintenance requirements. Hybrid and EV offer lower fuel costs but higher upfront prices.

- Set Annual Driving Distance: Enter your estimated annual kilometers. This is crucial for accurate fuel cost calculations. Higher annual mileage makes fuel-efficient cars more economical.

- Select Priorities: Choose what matters most: low running cost, high resale value, safety, comfort, or brand trust. The advisor scores cars based on your priorities.

- Get Recommendations: Click "Get Recommendations" to receive top 3-5 cars with detailed 5-year ownership cost breakdown, including fuel costs, insurance, maintenance, and resale value.

Understanding 5-Year Ownership Cost

Expand

Ownership Cost Formula

Our calculator uses a comprehensive formula to estimate true ownership costs over 5 years (and not just ex-showroom price):

Cost Components

- On-road Price: Ex-showroom price + road tax + registration + insurance (first year) + handling charges. Typically 10-15% more than ex-showroom price.

- Fuel Cost: Calculated based on annual kilometers, fuel type, and mileage. For EVs, uses charging cost per kilometer. Higher annual mileage makes fuel-efficient cars more economical.

- Insurance: Annual insurance premium × 5 years. Premiums vary by car model, age, and coverage type. Typically ₹25,000-₹80,000 per year depending on car value.

Pro-Tip: Standard insurance premiums are a zero-surcharge category. Paying your ₹40,000 annual premium via the SBI Cashback Card adds a direct ₹2,000 profit to your TCO. If you haven’t optimized your fuel spend yet, start with our Fuel Credit Card Guide.

- Maintenance: Annual maintenance cost × 5 years. Includes servicing, parts replacement, and repairs. Typically ₹15,000-₹30,000 per year depending on car brand and usage.

- Safety Multiplier (B-NCAP): We apply a safety multiplier in scoring based on Bharat NCAP (B‑NCAP) star ratings—safer cars tend to reduce “hidden cost” risk and often hold resale better in the real market.

- Resale Value: Estimated resale value after 5 years based on brand reputation and model popularity. Premium brands like Toyota and Honda have higher resale values (65-75% of original price) compared to others (50-65%).

If you’re deciding what monthly budget is “safe” for EMI + fuel + insurance, run your tax baseline too using our HRA Calculator.

Fuel Type Comparison

Petrol vs Diesel vs Hybrid vs EV

- Petrol: Lower upfront cost, moderate fuel efficiency (15-25 km/L), higher fuel prices (₹108/L in 2026). Best for low annual mileage (<10,000 km/year).

- Diesel: Higher upfront cost, better fuel efficiency (18-25 km/L), lower fuel prices (₹94/L in 2026). Best for high annual mileage (>15,000 km/year) and highway driving. Under CAFE III norms, diesel variants can see pricing pressure and may face softer long-term resale in some city markets as fleets shift to hybrids/EVs.

- Hybrid: Higher upfront cost, excellent city mileage (25-30 km/L), moderate highway mileage. Best for city-heavy usage and eco-conscious buyers. Lower fuel costs (at ₹108/L petrol) offset higher price over 5 years. Break-even typically at 12,000-15,000 km/year.

- Electric (EV): Highest upfront cost, lowest running cost (₹1-1.5/km at ₹9/unit charging in 2026), government incentives available. Best for city driving, low maintenance, and environmental benefits. Requires charging infrastructure. Resale value depends on battery health.

Case Study: Choosing the Right Family Car

Expand

Scenario: Family of 4 Looking for a Car Under ₹15 Lakh

Challenge: A family of 4 (2 adults, 2 children) needed a car for daily city commute (8,000 km/year) and occasional highway trips (2,000 km/year). Budget: ₹10-15 lakh. Priorities: Low running cost, safety, and comfort.

Solution: Used our Family Car Decision Advisor with: Family size: 4, Budget: ₹10-15 lakh, Usage: Mixed, Fuel: Any, Annual km: 10,000, State: Delhi (10% road tax), Priorities: Low running cost, Safety, Comfort.

Results (2026 fuel prices: Petrol ₹108/L, EV charging ₹9/unit):

- ✓ Top Recommendation: Maruti Grand Vitara Hybrid - 5-year cost: ₹19.2 lakh (includes ₹14.2 lakh on-road price + ₹3.9 lakh fuel costs + ₹1.25 lakh insurance + ₹75,000 maintenance - ₹9.1 lakh resale)

- ✓ Second Choice: Honda City - 5-year cost: ₹19.8 lakh (better resale value but higher fuel costs at ₹108/L)

- ✓ Third Choice: Hyundai Creta - 5-year cost: ₹20.5 lakh (higher fuel consumption in city with ₹108/L petrol)

- ✓ Key Insight: Hybrid car had lowest 5-year cost despite higher upfront price due to excellent city mileage (27.97 km/L) and lower fuel costs at 2026 petrol prices

- ✓ Fuel savings: Hybrid saved ₹1.4 lakh in fuel costs over 5 years compared to petrol equivalent (calculated at ₹108/L)

Key Takeaway: For city-heavy usage, hybrid cars offer the best value despite higher upfront costs. The 5-year ownership cost calculation reveals true value, not just purchase price.

Quick Wins for Common Scenarios:

Illustrative winners — run the advisor above for your state and budget.

| Scenario | Typical Winner | Example |

|---|---|---|

| City, 10k km/yr | Hybrid | Maruti Grand Vitara (case study above) |

| Highway, 25k km | Diesel | Tata Nexon (Diesel) — see advisor shortlist |

| Weekend, 6k km | Petrol | Honda City — see advisor shortlist |

Tips for Choosing the Right Family Car

Expand

- Consider 5-Year Cost, Not Just Price: A cheaper car with poor mileage may cost more over 5 years than a slightly expensive fuel-efficient car. Use our calculator to compare true costs.

- Match Fuel Type to Usage: For high annual mileage (>15,000 km), diesel or hybrid is more economical. For low mileage (<10,000 km), petrol is sufficient. EVs are best for city driving with charging access.

- Factor in Resale Value: Premium brands like Toyota, Honda, and Maruti have better resale values (65-75% after 5 years) compared to others (50-60%). This significantly impacts total ownership cost.

- Safety First: Look for cars with 4-5 star safety ratings. Safety features like ABS, airbags, and ESC are essential for family cars. Our advisor prioritizes safety-rated cars.

- Consider Seating and Space: For 4-5 members, a 5-seater is sufficient. For 6-7 members, consider 7-seater MUVs like Innova Crysta or Ertiga. Check boot space for luggage.

- Test Drive Multiple Options: Use our recommendations as a starting point, then test drive top 2-3 cars to assess comfort, driving experience, and features.

- Check Service Network: Ensure the brand has good service network in your area. Easy access to service centers reduces maintenance hassles and costs.

Why trust this calculator?

- 2026 fuel prices (petrol ₹108/L)

- State-wise road tax in the advisor form

- Brand-specific resale (e.g. Toyota 65–75% bands in our data)

- Typical Indian insurance & maintenance curves

Frequently Asked Questions

What is the break-even for Hybrid vs EV in 2026?

In 2026, break-even is driven by annual km and charging access. With Petrol ₹108/L and Diesel ₹94/L (April 2026 references), EVs usually win for city-heavy driving when home/work charging is practical, while hybrids often win for mixed/highway-heavy usage. As a rule of thumb, break-even often appears around 12,000–15,000 km/year—but your exact break-even depends on on-road price, insurance, resale, and your state’s road tax.

How much does it cost to own a car for 5 years in India?

A practical estimate is: On-road price + fuel/charging (5 years) + insurance (5 years) + maintenance (5 years) − resale value. For many family cars, 5-year TCO often ends up close to the on-road price (or higher) once fuel, insurance, and depreciation are included. This calculator runs it precisely for your state and usage using April 2026 references (Petrol ₹108/L, Diesel ₹94/L, CNG ₹82/kg).

Can I use a credit card for a car down payment in India?

Sometimes—if the dealer accepts it and there’s no surcharge or MCC restriction. Many dealers cap card payments or add a convenience fee. If a large swipe is accepted without extra charges, you can unlock outsized rewards and milestones (often worth ₹25k–₹50k). Always confirm acceptance limits and surcharges in writing before paying.

What is the easiest way to reduce fuel cost after you buy the car?

Start by locking in a fuel cashback card and tracking your monthly burn. Use the Fuel Credit Card Guide to pick a card that matches your city and pump network, then validate the savings with the Fuel Cost Calculator above.

Is it worth paying car insurance with a credit card in India?

Absolutely. Unlike down payments, insurance carries zero surcharge. Paying a ₹40,000 premium with the SBI Cashback Card nets you a flat ₹2,000 profit — making it the best credit card for car insurance premium 5% cashback available in 2026.

How to avoid the 2% dealer surcharge on credit cards?

Negotiate. Dealers often waive the surcharge if you opt for their in-house insurance or a service package. Alternatively, ask the dealer to raise an Online Payment Link — online processing fees are typically lower than offline POS machines. This is the most practical way to eliminate the surcharge on credit card for car purchase 2026.

What is the 45-day arbitrage hack for car buyers?

When you swipe your down payment on a credit card, your actual cash leaves your account only after the statement due date — typically 30–45 days later. During that window, you can park the equivalent amount (e.g., ₹5 Lakh) in a Liquid Mutual Fund earning ~7.2% p.a. via Upstox or Kotak 811. The interest earned on ₹5L over 45 days is roughly ₹1,562 — free money that reduces your effective TCO further. This is the core of the car loan vs credit card down payment arbitrage strategy.

Related Calculators

Calculate different aspects of your car ownership and fuel expenses:

- → Fuel Consumption Calculator - Calculate fuel needed for trips based on distance and mileage

- → Fuel Cost Calculator - Calculate monthly and annual fuel expenses with GST

- → Fuel Efficiency Calculator - Track your vehicle's kilometers per litre performance

Related Guides

Learn more about reducing fuel costs and maximizing savings:

- → Best Fuel Credit Cards in India 2026 Guide - Compare top 10 cards and save ₹8,000-₹14,400 annually on fuel expenses

- → Fuel Expense Documentation Guide - Master audit-ready record keeping and reconciliation workflows